How I Paid Off $10K of Debt Without Making More Money

How I Paid Off $10K of Debt Without Making More Money

What Happens If You Skip Paying One Credit Card Bill

Missing even one credit card bill payment can lead to unexpected consequences like late fees, higher interest rates, and a hit to your credit score—understanding these effects is key to keeping your credit card in good standing.

Posted by

Sable Monroe

Published

November 21, 2025

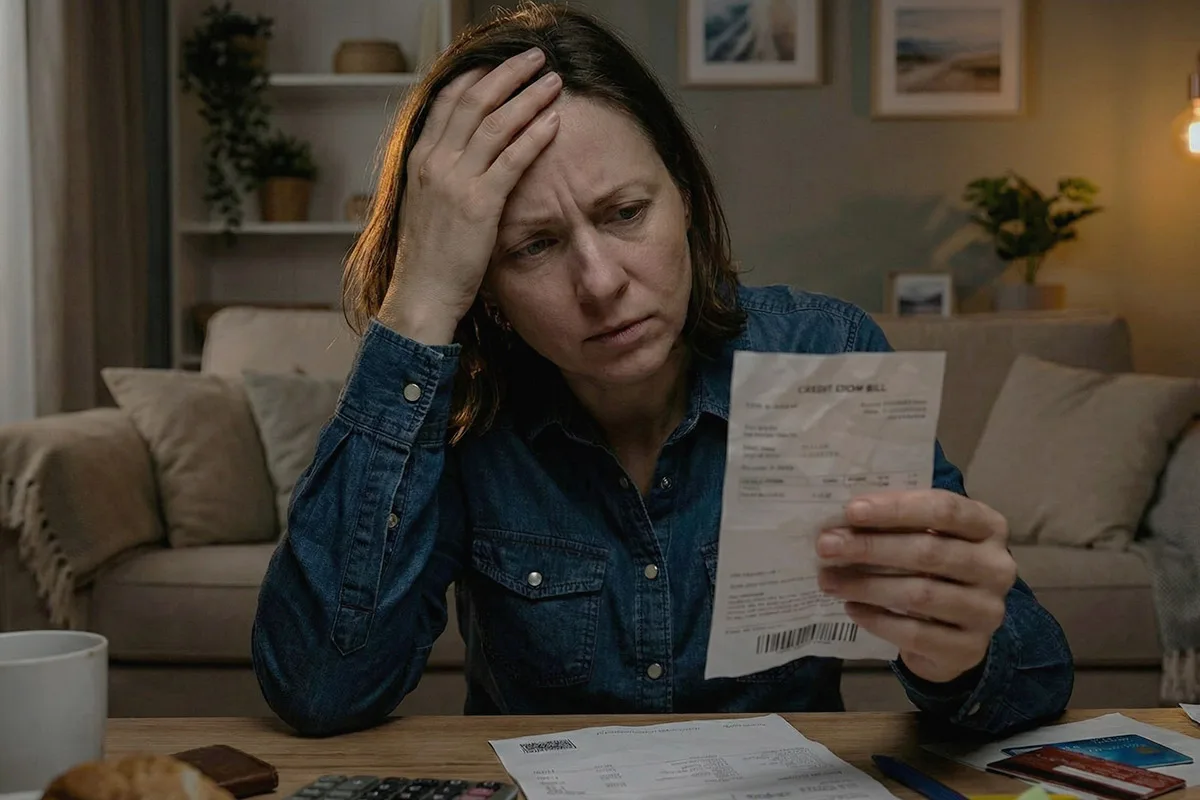

When managing finances, credit cards offer convenience and flexibility, but failing to meet payment deadlines can lead to unwanted complications. Missing even a single credit card bill payment may seem harmless to some, but the consequences can ripple through your financial life in several significant ways. Understanding what happens if you skip paying one credit card bill is essential to maintaining a healthy credit profile and avoiding unnecessary financial strain.

How Missing a Credit Card Payment Impacts You

Immediate Consequences of Skipping One Credit Card Bill

If you miss the due date for your credit card payment, the first impact you’ll notice is typically a late fee. Credit card companies usually charge a penalty fee, which can range anywhere from $25 to $40, depending on the issuers and your previous payment history. This fee adds to your outstanding balance, increasing the amount you owe.

Additionally, your credit card issuer will likely increase your interest rate. Many cards have penalty APRs, which can be significantly higher than your normal rate. This means that even if you pay off your balance afterward, any new purchases or carried balances will accrue interest at this elevated rate until you meet certain conditions, such as making timely payments for several consecutive months.

Effect on Your Credit Score

One of the most concerning consequences is the potential damage to your credit score. Credit card companies typically report late payments to credit bureaus after they become 30 days overdue. A single late payment reported can cause a noticeable drop in your credit score, which affects your creditworthiness.

The severity of the drop depends on your overall credit profile and how late the payment is. If it’s just one missed payment and you catch up quickly, the impact might be moderate. However, repeatedly missing payments or allowing accounts to stay overdue for longer periods can lead to a severe decline in your credit score. This damage can affect your ability to secure loans, rent apartments, or even get favorable insurance rates.

How Skipping a Payment Affects Your Credit Card Account

Missing a payment also puts your credit card account at risk. If you fail to pay your bill for several months, the credit card issuer may suspend or close your account altogether. In extreme cases, the account could be sent to collections, which compounds the negative impact on your credit report.

Moreover, the unpaid balance continues to accrue interest daily, often at a higher rate, causing your debt to snowball. This growing balance becomes increasingly difficult to pay off, leading to further financial challenges.

Fast Money Moves People Use to Tackle Debt Faster

When debt starts piling up, most people don’t overhaul their entire life — they look for simple ways to bring in a little extra money and gain momentum. One of the smartest tricks is stacking quick payouts from easy online tasks and putting that money straight toward balances. From short surveys to apps that pay instantly, these are some of the easiest ways people chip away at debt without feeling overwhelmed.

| Offer | Earning Potential | Task | Don’t Miss Out |

|---|---|---|---|

InboxDollars |

$225/month | Complete Surveys | Get Started |

FreeCash |

$1,000/month | Simple Online Tasks | Get Started |

Kashkick |

$1,000/month | Try Out Apps | Get Started |

Prime Surveys |

$300/month | Complete Surveys | Get Started |

Swagbucks |

$200/month | Simple Online Tasks | Get Started |

What To Do If You Miss a Payment

Missing a credit card payment can happen to anyone, and taking quick action can minimize the consequences. Here are some steps to consider if you forget or are unable to make a payment on time:

1. Make the Payment Immediately.

The sooner you pay, the better. If your payment is less than 30 days late, late fees and penalty APRs might still apply, but reporting to credit bureaus is usually not triggered until after 30 days. Prompt payment can help you avoid more severe penalties.

Debt Is Weighing People Down

See how they’re paying down balances with these 15 money moves >>

2. Contact Your Credit Card Issuer.

Many credit card companies are willing to work with customers who experience temporary financial difficulties. You may be able to negotiate a waiver for the late fee or request a lower interest rate if you explain your situation and have a good payment history.

3. Set Up Payment Reminders or Auto Pay.

To prevent future missed payments, consider scheduling automatic payments or setting up calendar alerts. These tools can help ensure bills are paid on time consistently.

4. Review Your Budget.

Missing a credit card payment may be a sign that your current budget isn’t working well. Assess your income and expenses to make adjustments that accommodate your debt payments comfortably.

Long Term Financial Implications

The consequences of skipping payments extend beyond immediate fees and credit score drops. Poor payment habits can make it harder to rebuild credit, especially if late payments become frequent. A damaged credit score can lead to higher interest rates on mortgages, car loans, and other types of credit in the future.

Additionally, the increased cost of borrowing due to penalty APRs and higher interest rates means you pay more over time. This situation can delay achieving financial goals such as homeownership, funding education, or saving for retirement.

Final Thoughts

Skipping one credit card bill payment may feel like a minor slip, but the consequences can accumulate quickly. From late fees and higher interest rates to a negative impact on your credit score, missing a payment introduces complications that affect your financial health in both the short and long term. The best approach is to make payments on time whenever possible and act swiftly if you realize a payment has been missed. Taking control of your credit card payments safeguards your financial future and maintains your ability to borrow at favorable rates when you need it most.

Posted by

Sable Monroe